On Thursday the Bank of England decided to put up interest rates once more as it continued to try to keep inflation under control.

It is the latest in a series of central bank decisions to increase interest rates in the last year or so.

But why – what does it mean for borrowers and savers, and what is likely to happen next? We explore some of these issues here.

– Why did the Bank of England raise interest rates?

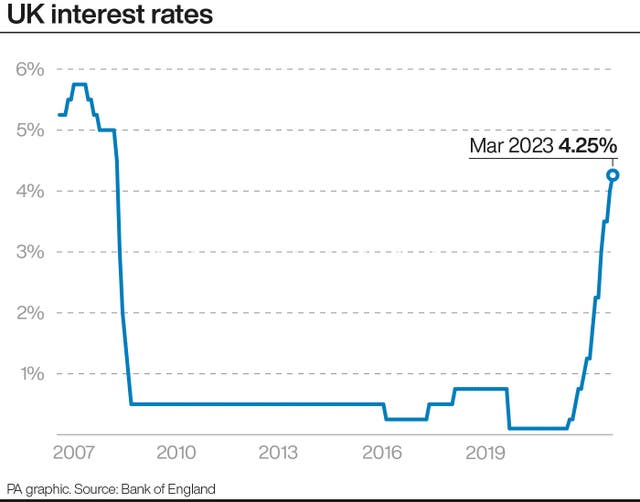

Bank decision-makers have been raising interest rates for around 15 months, with Thursday’s decision the 11th time in a row that policymakers have put the rate up.

Bank governor Andrew Bailey and his colleagues saw a ray of sunshine in the economy as they met this week – they expect inflation to fall quicker than previously and think the economy might just avoid recession.

This gave them a little more headroom to put up interest rates without worrying as much about the damage that might cause to the economy.

(PA Graphics)

(PA Graphics)

– What impact will this have on me?

The Bank’s base interest rate is what your bank likely bases your mortgage on – if you have a mortgage or are planning to take one out, that is.

So the rise will likely mean that people taking out a new mortgage, or whose mortgage is coming up for renewal, will see the interest they have to pay increase.

If – on the other hand – you are a saver who does not plan to borrow any money in the near future, this rate rise could help you out a little.

It will mean that the interest that your bank pays you on your deposits will rise, and other savings options will likely also offer more generous rates.

– Could this be the last time that my borrowing costs rise?

It may well be – many experts think so at least.

The Bank raises interest rates in order to help get inflation under control, and at the moment it very much looks like that will happen in the months to come.

There is still a chance that policymakers will have one final rate hike in May when they next meet – markets are only just pricing in a small rise.

The Monetary Policy Committee voted by a majority of 7-2 to increase #BankRate to 4.25%. https://t.co/3us4oE1pmh pic.twitter.com/uPn7ubt3Pa

— Bank of England (@bankofengland) March 23, 2023

– When is inflation going to get better?

It already is, and should speed up soon. Although it broke the trend in February, Consumer Prices Index (CPI) inflation has been steadily falling since its peak of 11.1% last October.

The Bank actually said on Thursday that despite the slight increase in February, it actually now expects inflation to fall faster than previously forecast between April and June.

This is largely because the Government decided to cancel a £500 per average household increase in energy bills. This alone will remove around one percentage point from inflation, the Bank said.

– What impact did recent problems in the banking sector have on the Bank’s decision?

The collapse of US lender Silicon Valley Bank (SVB) two weeks ago was in no small part because of rising global interest rates.

A decade of cheap money with low-interest rates had benefited the bank as the start-up scene blossomed in the US.

Trying to get a small return on the billions that customers had deposited in SVB accounts, the bank bought a pile of long-term bonds.

But when interest rates started to rise, its customers wanted better returns from SVB on their money. So it had to start selling these bonds, at a loss.

When word got out that it was struggling to meet these demands without taking a loss, it sparked a run on the bank.

Because of this, there was some speculation that global central banks might slow, or stop, their rate rises.

It put them in a difficult situation where on one hand they wanted to keep pushing down inflation, but on the other did not want to cause more pressure on lenders.

But the US Federal Reserve, the Bank of England, the Swiss National Bank and the European Central Bank have all hiked rates this week regardless.

Comments: Our rules

We want our comments to be a lively and valuable part of our community - a place where readers can debate and engage with the most important local issues. The ability to comment on our stories is a privilege, not a right, however, and that privilege may be withdrawn if it is abused or misused.

Please report any comments that break our rules.

Read the rules here